- What we do What we do

- How we can help How we can help

- Insights Insights

- About About

- Support Support

- Book a Demo

Lenders as Landlords?

There is more to getting in on the build to rent boom than just converting buildings into flats

Earlier this year Lloyds Banking Group, John Lewis and Boots all announced plans to enter the Private Rented Sector (PRS), with the plan to build an initial 11,000 new homes between them. The movement of major corporate entities into the lettings market offers them the chance to explore new revenue streams, but comes with new challenges and real risk to the reputation of these long-established brands.

An opportunity to attack a fragmented market

In different ways the traditional models of these businesses are under-threat: record low interest rates have squeezed margins for banks whilst Covid-19 has hastened the decline of the high street and physical retail. This has left these large organisations with both dwindling revenues and a surfeit of building stock.

In the age of the corporation, it’s also a major anomaly that the PRS is so fragmented with small scale landlords and letting agents dominating the market. The biggest lettings brand on the market, Connells, has just 14% market share, despite the recent takeover of one of its biggest rivals, Countrywide. Around 75% of the market is made up of SME-sized agencies serving small scale, and often private, landlords.

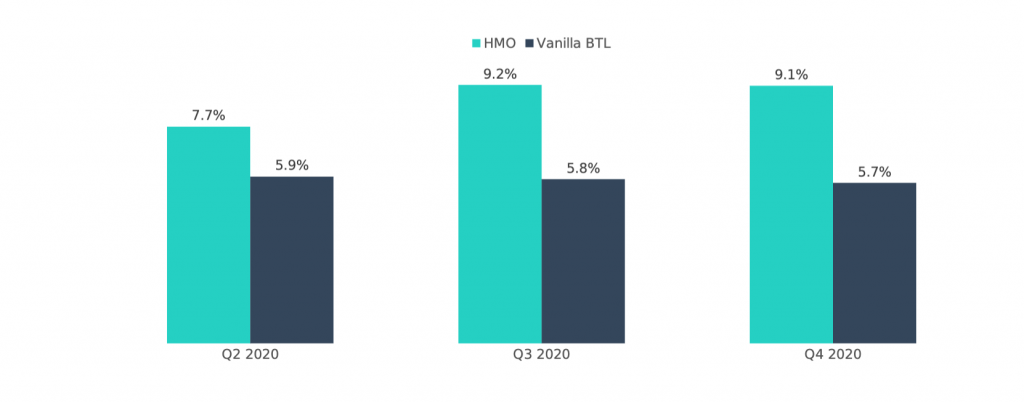

It is also a time of historical highs for the rental sector. Yields are reaching their highest level in years and the highest yield segment, HMOs, has grown beyond grubby student lets to offer accommodation that is often closer to serviced apartments. It’s no surprise to see a lender with <2% interest rates longingly looking at the 6-9% yields available to landlords.

Average gross yields on rental properties – by type

A high margin market with no dominant leader looks ripe for targeting by those with impressive brand reputations. These new entrants can deploy substantial benefits of scale and have proven expertise in managing large, complex businesses and estates. They have also built considerable consumer trust and brand credibility. All together this makes them a formidable competitor for incumbents. It is also expected that their portfolio could include homes on sites vacated by branches, making use of distressed inventory to build both new revenue streams and the high quality homes that the UK needs.

Regulation a threat to reputation

The big challenge is that these businesses have little to no experience in several core areas: letting, marketing or managing property, and they’ve chosen a particularly challenging time to start. Regulation is at an all-time high, leading to tax advisory firm Blick Rothenberg issuing warnings to Lloyds and John Lewis regarding their entry into the PRS:

“The legislation governing the rental of UK properties has become increasingly complex. New entrants to the market need to consider whether they employ an in-house team or outsource the management of their properties… it is not simple, and it can go wrong.”

The market is so complex that leading agents are even deploying compliance management as a unique selling point (USP) to impress landlords and win more business.

“Kamma has helped us stand out from other agencies because we’ve been able to be more prepared [in dealing with regulatory compliance]… We’ve been able to stand out purely by being the best at compliance in our area.”

-Ellie Donaghy, Head of Lettings, Andrews Property Group

If compliance is complex and important enough to drive market share, it surely warrants close attention from these new players.

So what does a new landlord like Lloyds have to contend with? One big challenge is in the area of property licensing where locally managed schemes create a complex web of rules to follow. With regulations changing on average every 8 days, and with mandatory and discretionary licensing overlapping it becomes very difficult to keep up.

The costs for getting it wrong are also material. Fines of up to £30,000 quickly erode available margins on entire portfolios, whilst delivering real reputational damage to big brands that have a lot more to lose. Lloyds is a household name and has spent years building up the corporate image to go with it. Thanks to a sustained, multi-million pound investment over several years, the image of a black horse is now synonymous with a lifetime of banking support. But, as Warren Buffet famously said: “It takes 20 years to build a reputation and 5 minutes to ruin it.”

Property is on a Path to Net Zero

There are also major challenges on the road ahead linked to energy efficiency and household emissions. Residential property contributes around 21% of UK emissions and most homes are considered energy inefficient. The UK government recently passed the first reading of a Bill that would see lenders having to average EPC grade C by 2030. The measures for the PRS are even more aggressive with the Minimum Energy Efficiency Standard of all rental properties increasing from an EPC grade E, to a grade C. In effect this means around 60% of UK housing stock would no longer be eligible for lettings. In the rush to re-develop distressed inventory in the form of retail outlets, these new players need to be sure to stay ahead of changeable legislation. For those already being targeted by activists for association or investment in environmentally unfriendly activities, the media will be sure to keep a close eye on their green credentials.

Lenders already have substantial challenges linked to the energy efficiency of their mortgaged portfolios:

In short, those with decades-old reputations that are about to enter the PRS would do well to consider the serious pitfalls that come with the fines associated with non-compliance, the bad press of dissatisfied tenants and the major challenge of upgrading UK housing stock to meet Net Zero targets. To truly take advantage of the opportunity ahead of them, whilst also avoiding these pitfalls, expert partners, data-driven decisions and market-leading RegTech software is needed. Kamma is, of course, happy to provide all three.

Contact us or book a demo now to understand how Kamma can solve property licensing for you.

How EPC data impacts property valuation for mortgage lenders

Reliable and up-to-date energy efficiency data is a must to ensure an accurate property valuation for UK mortgage lenders – here’s why.

Read more

New insights: how does EPC data impact affordability assessments?

Accurate energy performance data is a must to ensure mortgage lenders can accurately assess affordability and reduce risk – here’s why.

Read more

Kamma’s Response to CVE-2024-0394 (XZ Utils Backdoor)

Last week security researchers publicised a malicious back door in the XZ Utils library, a widely used suite of software that gives developers lossless compression and is commonly used for compressing software releases and Linux kernel images. The backdoor could, under certain circumstances be used to run unauthorised code via the encrypted SSH connection protocol. […]

Read more

Subscribe to the Kamma Newsletters

Regular news, information and insights from Kamma. No spam. Unsubscribe at any time.

Subscribing ...

Sorry, we really want to but we couldn't subscribe you due to missing or incorrect information; please update the information that's highlighted in red and try again.

Well this is awkward. Something went wrong on the internet between your browser and our newletter subscription service. Please let us know and we'll do our best to fix it for you.

Thanks for subscribing! Check your Inbox in a short while for a confirmation email to check it was really you that just subscribed. If you've already subscribed, we'll keep your subscription but you won't receive a confirmation email this time.