- What we do What we do

- How we can help How we can help

- Insights Insights

- About About

- Support Support

- Book a Demo

Is a green storm coming to the UK?

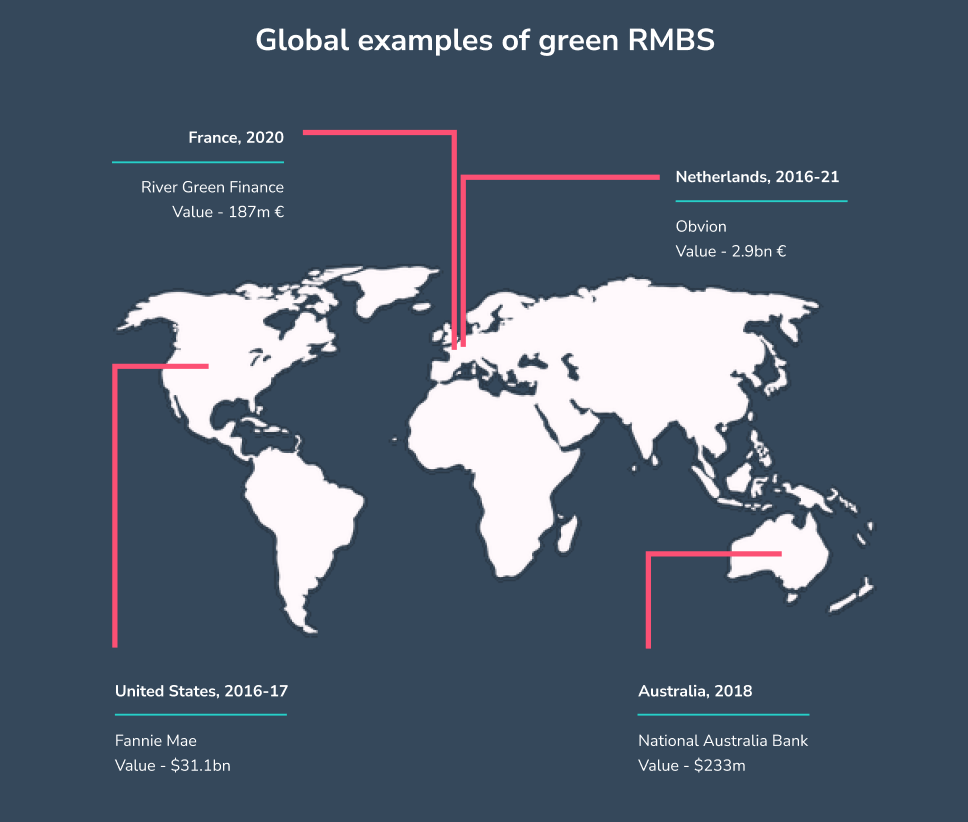

On the 4th June GlobalCapital broke the news that Kensington Mortgages had announced the UK’s first ever green Residential Mortgage-Backed Securitisation (RMBS), some five years after the world’s first launched in the Netherlands. The Dutch international cooperative bank Obvion, is a subsidiary of Rabobank – the Netherlands largest mortgage lending business, with a lending portfolio directed towards retail customers and corporates. Obvion has actively been investing in the Dutch housing market for more than 30 years and are known for their commitment to the country’s transition towards a sustainable economy.

In 2016, Obvion developed the ‘Green Storm’ green bond framework under which it issued the world’s first 100% green mortgaged backed securitisation. Green qualification was confirmed through two routes: all underlying assets included in the bond were from energy efficient residential mortgages whilst the use of proceeds was directed towards the financing of further green mortgages. Such was the success of the launch that Obvion has continued to release a new green RMBS on an almost annual basis.

Green securitisations issued by Obvion

| Obvion | EUR 526.2m (USD 595.1m) | Netherlands | 2016 |

| Obvion | EUR 526.2m (USD 595.1m) | Netherlands | 2017 |

| Obvion | EUR 587.8m (USD 687.9m) | Netherlands | 2018 |

| Obvion | EUR 641.3m (USD 722m) | Netherlands | 2019 |

| Obvion | EUR 531.7m (USD 636.4m) | Netherlands | 2021 |

| Total value: EUR 2.88 billion |

How did Obvion qualify mortgages as green?

The 2016 Green Storm pool contained energy efficient homes and houses that had been refurbished to improve energy efficiencies. The Dutch EPC rating system is a result of the government’s implementation of the revised 2010 EU Energy Performance of Building Directive. Similarly, to the UK, the EPC rating of a property is rated from A to G, with A representing an efficient property and G inefficient.

How properties qualify as green in the Netherlands (2016-2020)

- Buildings that have obtained an EPC of A or B by the Netherlands Enterprise Agency.

- Buildings with a definitive EPC C or higher that have demonstrated an improvement of two grades in their EPC grade.

Obvion measured against this criteria by address-matching properties in the bond with externally provided EPC data from the real estate data company Calcasa. The Netherlands Enterprise Agency is the original source, tasked with maintaining records for the entire country’s properties.

Sustainalytics, acting as second party opinion provider further verified the compliance of Green Storm 2016 with the use of the Low Carbon Housing Standards of the Climate Bond Initiative.

Updates to the Obvion green framework in 2021

Since the first launch in 2016, Obvion has continued to develop their in-house green bond framework under which it issues securitisations. The frameworks determines eligibility criteria in three key areas:

- Residential buildings built before 2021 that have a definitive or provisional Energy Performance Certificate (EPC) of at least A by the Netherlands Enterprise Agency.

- Residential buildings built as of 2021 with an EPC grade of A++++ (a new level of rating brought in for properties with a net primary energy demand at least 20% lower than required for Nearly Zero Emission Buildings (NZEB))

- Residential buildings with a rating of EPC B, or C, that have demonstrated an improvement of at least two grades.

How successful was the 2016 Green storm securitisation?

After the launch in 2016, Max Bronzwaer, Executive Director and Treasurer of Obvion commented

“The order book was over EUR 1.2bn so it was no problem to fully allocate this green RMBS to green investors”.

A green securitisation based on both green underlying assets and green use of proceeds, sold only to green investors represents a step change in the function of the market and highlights the great investment demand for green bonds and securities. Since 2016, Obvion has issued green mortgaged backed securities on an almost yearly basis, delivering a running total of over €2.9 billion in green securitisations to market in the last five years.

The future of green securitisations in the UK

Is 2021 the year we can expect a green storm in the UK?

Lenders in the UK are under increasing pressure from the government, regulators, investors and their own customers to increase their efforts in reducing both their own environmental footprint, and those of the homes they invest in. More accurately matched EPC data offer lenders the opportunity to issue their own RMBSs and lead the market in green lending.

By using address-matched data to qualify the underlying assets, and then reinvesting proceeds in green projects, Obvion were able to double qualify the securitisation as green, side-stepping challenges around lack of a single agreed definition of green. Importantly, this also kickstarted a virtuous circle, with recapitalisation used to fund further green mortgage loans which led to further green securitisations.

Lenders could deploy green securitisations in the same way here in the UK, with freed up capital supporting smaller scale green projects and improving the average energy efficiency ratings of their mortgaged assets. With an estimated 3 million homes in the UK at EPC A or B, the opportunity to kickstart a similar green lending revolution is much larger. The UK is also home to some of the world’s leading experts in geospatial technology.

With the use of geocoding, EPC data, and further government regulations around sustainable bonds, UK lenders now have all the data and instruments needed to launch their own green securitisations, creating a green storm of their very own.

Download our free report to uncover the opportunities for lenders in the transition to net zero.

New insights: how does EPC data impact affordability assessments?

Accurate energy performance data is a must to ensure mortgage lenders can accurately assess affordability and reduce risk – here’s why.

Read more

Kamma’s Response to CVE-2024-0394 (XZ Utils Backdoor)

Last week security researchers publicised a malicious back door in the XZ Utils library, a widely used suite of software that gives developers lossless compression and is commonly used for compressing software releases and Linux kernel images. The backdoor could, under certain circumstances be used to run unauthorised code via the encrypted SSH connection protocol. […]

Read more

Licensing Compliance Simplified: The Kamma-Reapit Integration

The Kamma app is officially live on the Reapit marketplace! This integration arrives just in time to confront the introduction of fifteen new licensing schemes and six current consultations in the first half of the year alone. Kamma’s Reapit integration empowers you to effortlessly manage your licensing compliance through: How does the app work with […]

Read more

Subscribe to the Kamma Newsletters

Regular news, information and insights from Kamma. No spam. Unsubscribe at any time.

Subscribing ...

Sorry, we really want to but we couldn't subscribe you due to missing or incorrect information; please update the information that's highlighted in red and try again.

Well this is awkward. Something went wrong on the internet between your browser and our newletter subscription service. Please let us know and we'll do our best to fix it for you.

Thanks for subscribing! Check your Inbox in a short while for a confirmation email to check it was really you that just subscribed. If you've already subscribed, we'll keep your subscription but you won't receive a confirmation email this time.